By Livia Caligor March 31, 2021

Malia Mills swimwear, which celebrates body inclusivity and empowerment with its attention to fit, comfort and high-fashion aesthetic, pioneered an untapped market and galvanized industry attention, and has since expanded to cover-ups, draped dresses and rompers, blouses and trousers, in addition to swimwear. Within just a few years, Malia Mills swimwear was available through wholesale distribution at over 125 specialty stores across the globe, from Barneys New York and Neiman Marcus to Aman Resorts.

by Isabelle Pappas

Everyone has said that this year’s presidential election is the most important one of our lives. And yet, it seems that we’re all regarding it as one big joke, with many memes resulting from various campaign rallies and presidential debates.

by John Colie

Editor’s note: Historical information from this article comes from two main sources: “Our Most Vulnerable Election” by Pamala Karlan, published in the New York Review of Books, and The Complete Book of U.S. Presidents by William A. DeGregorio. By the time this article is published, we might have a slightly better idea of how this year’s presidential election might turn out.

By Harry Ducrepin

The presidential election is coming up in a few days and thinking about the consequences of America’s choice next Tuesday is both devastating and overwhelming. I’ve spent the past week or so trying to clear my head of the realization of what could soon become reality.

by Dylan McIntyre

Let’s face it: the world’s in a really bad place right now. America has never been so divided, and with the upcoming election, all of this country’s divisiveness will come to a head.

by Dylan McIntyre

Online education is a pretty polarizing topic nowadays. Most of us are experiencing it firsthand, and after several months of using Zoom, chances are you either love its flexibility and leniency (how else would I get to attend lectures in pajamas?) or you just want to throw your stupid laptop out the window because your background image has been permanently burned into your retinas.

by Isabelle Pappas

The class of 2025 will be applying to college in the midst of a global pandemic, and Cornell has chosen to relieve the single most stressful aspect of the college application process: standardized testing. The Sun reported back in April that Cornell would be the first Ivy League institution to waive the standardized testing requirement for both early and regular decision applicants in this year’s admission’s cycle.

by Dylan McIntyre

Let’s face it: making friends at college is hard. Adjusting to life on a college campus can be a real challenge, and in COVID times, these challenges have only grown.

by Isabelle Pappas

The method of college reopenings around the globe has been under public scrutiny during these initial weeks of the fall semester. Admins and students alike are being assessed on their ability to resume in-person instruction safely when very limited physical interaction is even deemed safe.

by Harry Ducrepin

The American prison system is incredibly flawed and unjust, but this is something we all already know. When we talk about problems in the system, the same ideas pop up, notably the privatization of prisons, mass incarceration and lack of rehabilitation programs. While it’s great that we have acknowledged these issues, we should start to think beyond the scope of them and get a little more radical.

by Katriana Galloway

You’re rotting. Your brain is shriveling, and your body is shrimping.

A candid conversation with FSAD alum Gizelle Begler ’08 about establishing her namesake couture label, destigmatizing the hijab and utilizing fashion as a vehicle for social change.

Compiled and written by Livia Caligor

As Toni Morrison shared with The Guardian in 1992, “In this country American means white. Everybody else has to hyphenate.” In a riveting dialogue on the implications of the African-American identity, she begs her readers to question what it means to be hyphenated, how it feels to be considered American by law but a second-class category of citizens by practice.

Stars: They’re just like us! There’s something comforting in knowing that I’m not the only one who has to stay home and at a six feet distance.

by Zachary Lee

With commencements and graduations nationwide either being cancelled or going virtual, the Veritas Forum is ensuring that before the year ends, members of the Class of 2020 still get to share their stories. The organization, which places historic Christian faith in dialogue with other beliefs and invites participants from all backgrounds to pursue Truth together, has partnered with The Augustine Collective and Comment Magazine to launch the #My2020CommencementSpeech Contest, which will publish five commencement speeches written by graduating seniors.

Unless you’ve been living under a rock (in which case, don’t move), you know the importance of self-isolating to protect yourself and others during the coronavirus pandemic. We might be stuck at home, but we need not succumb to boredom.

Hardly a couple weeks ago, while still a student in the traditional sense, I observed the bespeckling of our once-tangible institution by a scattered but substantial population of a particular type of student. For the sake of your efficient recollection, I’ll attempt to compile them all into a cast of two characters (they aren’t a terribly varied crowd).

Paying absolutely no attention in an econ discussion section is student number one, daydreaming about enlisting in the active troops of America’s dumbest youth currently deployed on Miami beaches.

[Content warning: this article contains discussion of body image. Reader discretion is advised]

I was shocked when I got home and realized I had gained 15 pounds.

Don’t have a Goodwill near you? Can’t afford to independently wear down some white sneakers via walking in them, as one does?

Anyone who publicly professes their love for the hit series The Bachelor is bound to be immediately met with rolling eyes, judgmental smirks, and questions that sound like, “You don’t seriously watch The Bachelor right?”

Yes, yes I do. And proudly, as well.

In a world of increasing specialization, students of the University often feel pressured to narrow their paths of study. Business major, English minor and chimesmaster Sonya Chyu ‘18 was a joyful exception to this rule.

It’s the most eccentric, trailblazing and radical time of the year! Aquarius is ruled by Uranus, the planet of freedom, originality, rebellion and revolution.

I am holding a paper sign that says, “Because over 90% of LGBTQ tech employees surveyed reported experiencing harassment, mistreatment, or discrimination at work,” inside the intersection of Duffield Hall, where Women in Computing at Cornell (WICC) took a picture for their Fall 2019 Diversity Photo Campaign, #ILookLikeAnEngineer. Discovering my passion in Computer Science & Information Science

By the time December 26th rolls around, Instagram was suddenly flooded with memes revolved around the new year: Confessions of how awful 2019 was. Proclamations that 2020 will be the year.

December 22-January 20

It’s Capricorn Season! That’s code for: time to get your sh*t together!

By xylyls November 26, 2019

Will prepares a birdseed taco for a ruminative Bird.

Founded in 1973 in memory of benefactor and Cornell Trustee Herbert F. Johnson (Class of 1922), the Herbert F. Johnson Museum of Art is home to over 35,000 permanent works of art. Its diverse collections span six millennia and a wide spectrum of cultural origins.

November 22 – December 21

How did Scorpio season treat you? Did you barely escape the murky waters alive?

Check-in time! It’s about halfway through the semester at this point, and everyone’s favorite time of year: flu, prelim, and snow season.

What many people don’t know is that having access to Cornell’s fitness centers also means having access to an array of group fitness classes – not just taught by elderly and overweight ex-PE teachers, but also your overly enthusiastic but super strong peers. Luckily, these classes span gyms across campus and boast tons of time slots – perfect for your 7 am Yoga or 7 pm HIIT.

By xylyls November 17, 2019

[This is the first installation of the comic series BIRD & human. Enjoy.]

In an effort to escape running into a recent ex, Bird takes a detour across campus.

Anyone who has binge-watched Modern Family, Full House, or any other family based sit-com can admit to laughing loudly at situations, while simultaneously smirking and thinking “this would never actually happen…”

I’ll admit, I once believed this too. The events in those shows seem too scripted to ever actually happen.

We all remember the moment at the 2016 Met Gala when the lights dimmed, red carpet chatter silenced into hushed gasps, and heads turned to see Claire Danes step out in a ball gown that shined brighter than the explosion of camera flashes that quickly ensued. The whimsical piece constructed out of sheer organza and fiber optics was the fashion moment of the year — the LED gown fused other-wordly glamour with contemporary polish, a timeless silhouette with cutting-edge technology, and could only have been a creation of the legendary Zac Posen. I was immediately infatuated with his ceaseless passion for experimentation and

innovation — each custom gown jaw-dropping in a new way — paired with his unwavering vision as an artist, each piece unmistakably his.

In case you live under a rock, or, like some mysteriously sane person, don’t check social media, you might have missed the “Due Friday” memes that went around last week. What a wonderful way for students across the entire university to come together and do what we do best: 1) roast the f*ck out of each other and 2) poke fun at how busy, stressed, and depressed we all are. See below for my top picks from the notorious “Any Person, Any Meme” Facebook group…

17.

Happy Halloween and Happy Spooky SZN! It’s no coincidence that Halloween (and every U.S. presidential election) falls when the sun is in Scorpio, the most mysterious, scary, and downright frightening of all 12 Zodiac signs.

There’s something about throwing up a janky peace sign to yourself in a greasy mirror post-weekly Wednesday night sobbing session (no, not the one you had scheduled in your G-Cal that should have ended forty-five minutes ago, the one that came after you hit that point in the night where you realized it was an all-nighter kinda night) that gives you the strength to wash off your runny mascara that you paid an extra ten dollars for and wipe off the remnants of the half a gallon of chocolate milk you impulsively bought at Jansen’s twenty minutes ago (even though you’re lactose intolerant and wanted to go Vegan three days ago) and walk back into the Cocktail Lounge. I know what you’re thinking, “wow, Sara, that’s like really messy, maybe you should see someone” or “maybe just stop buying the chocolate milk?”, but I sweaarrr it’s totally not about me, and if it was, I’m only sometimes lactose intolerant.

We all get a warm feeling when we see the Friends cast laugh together as “I’ll be there for you” plays in the background… because they really will always be there for us. No matter how lonely or bad we’re feeling, we can always count on the Central Perk squad from the world’s most popular sitcom to cheer us up…

I certainly counted on Friends being just a couple of clicks away my entire first week at Cornell, since I was homesick and everything outside of the four walls of Bauer Hall seemed scary.

Last spring, I took the 6 train from the periphery of Spanish Harlem to my office in Soho every day. I remember the way I’d limp up the hill at the cross section of 110th Street, peering into the backlit shadow of the subway stop at the end of the street, blasting Bowie classics to cancel out the whisper of catcalls around me.

By xylyls October 18, 2019

I try to catalogue everything that happens, maybe to the brink of obsession. To that point, I have three pillars on which I rely to retell what is effectively my story: my Google calendar, a five-year Hobonichi, and my bullet journal.

Given there are exactly 12 candidates vying for the Democratic nomination at tonight’s debate, I figured I had to highlight them all as represented by the 12 Zodiac signs. (Admittedly, I know way more about astrology than I do about politics- don’t come after me!)

Elizabeth Warren: Aries

Known to “swat and jab at the air” in interviews, Warren can seem a bit Aries Aggressive indeed.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, October 21 edition of the paper.

So recently I found myself in a tragic, embarrassing situation that may as well be straight from a viral college tweet. I mean, take the infamous “I am worried” email sent to a professor and multiply the awkwardness by twenty to get something near the level of cringe of my situation.

Every September 23rd, we say farewell to Virgo season. We express our gratitude to the ever-so orderly and rule-abiding Virgin for getting us back on track after that wild Leo end of the summer 🙂 Alas, Virgo brought us back down to Earth- and back to the library.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, September 23 edition of the paper.

Dear Mom & Dad,

How are you? Is the sun shining?

Welcome to the first installment of a 12-part series highlighting each Zodiac sign! In my opinion, astrology has fascinating implications that may guide us toward manifesting our greatest, fullest, and highest selves in the sacred time we have on this Earth.

Pack your schedule to the max

One of the great things about Cornell is that they are well aware of the difficult transition between high school and summer to living at college, and they go through a lot of effort to make the change as easy as possible for incoming freshmen with Orientation Week. Events start as early as the day of move-in, and if you take full advantage of the university’s scheduled activities, you shouldn’t have a single minute of empty time to stew over the discomfort of being in an entirely new and unfamiliar place.

We get it! You probably have a lot of questions.

For a period of time in my childhood, I thought Cornell was the only college. I didn’t understand the concept of a University, but I had also been conditioned well.

Writing about endings tends towards the cliché. I want to preface this by saying that it’s impossible for me to write about graduation without feeling uncomfortably self-aware of the redundancy of my feelings.

Songs for May 9

Act 1: Father John Misty – “Nancy From Now On”

Nothing says ‘How did I end up asleep on my friend’s porch?’ quite like a Father John Misty song.

Act 2: The Fray – “How to Save a Life”

Walk home.

Thanks for a great year of great captions! Feel free to submit a caption for the first paper of next semester.

Confession time: I am that annoying girl in your math lecture that obnoxiously munches on ice the entire time. But honestly, how could I not?

Have you ever had to sit segregated from your group of friends in lecture? Have you ever had to walk into a classroom and step over countless feet on your way to the most inaccessible corner of the room?

In case you missed Part 1 and Part 2 of this series, you can scan through my complete, updated Top 50 list for a quick refresher. This final group of players was so hard to rank that, after losing nights of sleep over it, my dad suggested that I go back to my original criteria for ranking players: “If you dropped this player onto any NBA team at random, by how much would they improve that team’s odds of winning the title?” I set up a spreadsheet with each of the remaining players as the columns and all the playoff teams as the rows, and I tried to estimate (as best I could) the increase in championship odds if each player were to be magically placed onto each team’s roster.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 29 edition of the paper.

I am here to send out a PSA to all those suffering from FOMO and all those suffering because of the people who suffer from FOMO. For those of you who do not know, FOMO stands for “Fear Of Missing Out.” A common occurrence in many friend groups, one of the most frequent cases is when someone suddenly finds out they were not invited to an event that their friends went to together, either through social media or word of mouth.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 22 edition of the paper.

By now, we’ve all learned that almost anything can be political. As public discourse is integrated into industry and culture, it’s almost unusual for a company to lack a hot political take or sympathetic philanthropic cause.

Q: So it’s going to be the end of the semester soon, and I have a problem: I’m a freshman, and I feel like I don’t have strong, sustainable friendships. My roommates are nice, but I don’t see us hanging out much after this year, and I’ve got some platonic friends from my FWS, but once that’s over, I have no idea if we’ll still talk to each other.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 15 edition of the paper.

I often wonder what people think of me when they look at my Instagram profile. Do they think that I’m 10/10 awesome?

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 8 edition of the paper.

Felicite Tomlinson, sister of former One Direction member Louis Tomlinson, died suddenly on March 13th at only 18 years old from a suspected heart attack – a reality being “increasingly recognized in young women”, according to Professor Simon Redwood, a consultant cardiologist at London Bridge Hospital. And Felicite isn’t the only one.

A close friend of mine once told me to seek discomfort. Actually, that’s not true at all.

You’re walking straight down College Ave. and find that someone else is walking straight at you.

The night Captain Marvel was released, my friends and I drove to the Ithaca Mall movie theater in a car, brimming with anticipation. Though I don’t consider myself a die-hard Marvel fan, I was particularly excited to see this film—the CGI effects and female-driven storyline captivated my attention.

Here I hand to you a figurative racket to bat back those mental health grenades. Everything is going to be fine.

They won two Billboard Music Awards, performed at the American Music Awards with their hit song DNA, and recently attended the 61st Grammy Awards to present the award for Best R&B album to artist, H.E.R. Surely you must have heard of them. BTS, also known as Bulletproof Boy Scouts when they first arrived on the Kpop scene, is one of the most famous boy groups to attract international audiences.

“The American dream has become something much more closely resembling a nightmare, on the private, domestic, and international levels.” — James Baldwin, The Fire Next Time

Screw quinoa, berries and especially whole vegetables. The newest health trend: celery juice.

Over the course of the past couple weeks, the BDS (Boycott, Divest, and Sanction) movement has been a particularly hot topic on campus. From initial communications between SJP (Students for Justice in Palestine) and Martha Pollack to an uneasy session of the Student Assembly, the issue has taken center stage for many campus organizers and members of student government.

Black History Month is an annual celebration of achievements by black people and their role in history. Since 1976, February has been designated Black History Month, not only in the USA, but in countries around the world- including Canada and the United Kingdom.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, March 11 edition of the paper.

I have a confession: I’m an addict. The feeling I get when I succumb to the sweet, constant pull is utterly indescribable.

Last week, I was making conversation with a customer during one of my work shifts. She was speaking about a vegetarian friend, who was shaming her friends for their decision to eat meat.

Okay, I’m going to assume you’re behind on your work. Way behind.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, March 4 edition of the paper.

By Lev Akabas February 16, 2019

The dunk contest was my favorite night of the NBA season as a kid, to the point where I would count the days down from months away until I would get to watch the most athletic players in the league see who could jam a basketball into the hoop in the coolest way. Many years after I reenacted every single dunk contest dunk on my NERF hoop, something about the event continues to enthrall me, so I’m handing out awards for the bests and worsts in dunk contest history.

New, original crosswords will appear monthly.

Solutions:

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, February 18 edition of the paper.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, February 11 edition of the paper.

Before people get mad, let me just say that I’m extremely grateful to have access to Cornell’s diverse dining options. Some of my friends back home only have one dining hall, so we are lucky to have six on West Campus, alone.

Millions of Americans have been affected by the government shutdown, and many workers’ livelihoods are at the mercy of the decisions of powerful elites. While witnessing the news about the American government shutdown, another shutdown occurred in my home country of Zimbabwe.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, February 4 edition of the paper.

Meet us halfway and submit a caption for the first cartoon of the year! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, January 28 edition of the paper.

If you’re interested in which guys were 27 through 50 on my list, my criteria for these rankings, or the meaning of the different statistics I’m referencing in this article, check out Part 1. Additionally, after flubbing some players’ rankings in Part 1, I’ve decided to keep my Top 50 in a Google Doc, so that I can both correct my previous mistakes and continue to update the list throughout the season.

By Lev Akabas December 28, 2018

We know how to rank teams: my team beats your team, therefore my team is better. Just rooting for our teams carries an old-school sense of hometown pride and loyalty, but ranking players is overwhelmingly more interesting and fun — it’s a combination of statistics and intuition, of situational evidence and conjecture.

Disclaimer: I formally recognize economic, racial, knowledge, gender, and every other sort of privilege as ongoing problems that we should all strive to become more cognizant of, as they have and continue to create inequality that provides for unjust pain and suffering. This article is my opinion on privilege on a much smaller scale within my personal experience.

Congratulations to the winner of Cartoon Caption Contest #19! “I’m sorry I must go!

This past weekend was quite the ride. I visited SUNY Upstate Medical University for a PATCH (a pre-health organization I’m part of) field trip, taught for a program called Splash!, and ran the Syracuse Half-Marathon.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, December 3 edition of the paper.

One must still have cows within oneself to be able to give birth to a dancing star. -Friedrich Nietzsche

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, November 19 edition of the paper.

About a week ago, I watched this video:

And my goodness, did it make me think of Cornell. Anna Akana is a Youtuber, life guru, and mental health advocate who creates videos about relatable and relevant topics, as well as longer narrative films. In this particular video, she discusses how impossible it feels to be happy when it seems as if your whole world is on fire — a sentiment that many Cornellians share on a weekly basis.

In the past week I have napped an average of two hours per day, impulsively bought three sweaters that I cannot afford, practically inhaled Twizzlers and an entire sleeve of Oreos, and watched five of the raunchiest past episodes of The Bachelor, all while telling myself, “It’s called self care.”

Hindsight is 20/20 of course, and looking back I think my actions were probably the complete opposite of self care. In the moment, however, I was so encapsulated in my stress from prelim season that I allowed myself to do practically anything just because I have this extremely vague mantra to “affirm” my desires.

‘Tis the season of campaign ads, mudslinging, robocalls, selfies of people with their “I Voted” stickers, and all of those other wonderful things that go along with election season. Let us all be grateful now that the ballots have been cast, and it’s over: our social media feeds can live in peace, for a moment.

There’s a time and a place for guilt. Most times it’s within reason—after doing something immoral, unethical, or unkind, it’s a necessary part of self-regulation that, without intention, keeps our emotions in check and subsequently provides a feedback mechanism for changing or continuing a behavior. Psychology Today assembled a short list of five types of guilt and how to cope with them.

Alcohol Use Disorder

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, November 5 edition of the paper.

Set your alarms to 7:00 a.m. sharp. Spring pre-enroll kicked off today for seniors, and the rest of campus isn’t too far behind.

Confessions of a Serial Napper

It’s the end, beginning, or maybe smack dab in the middle of a very long day. You’re trying to do your work, but your eyes feel heavy and you begin to droop.

Over 146,000 people—myself included—find Instagram user @yrsadaleyward absolutely beautiful. She’s got impeccable taste in fashion, gorgeous hair, and an uncanny talent for combining messy colors to create the perfect aesthetic.

I spent last semester studying in the far-off land of New Zealand. Now I’m back and it’s time for that self-hatred inducing study abroad post where I tell you how I made meaning out of fleeing the country for a little bit.

The two movies pictured above have set off a wave of Asian and Asian-American embracement both cinematically and across the internet that has given hope to millions of Asians, myself included, who finally get to see people who look like them in roles other than the stereotypical Harvard (blegh) nerd with humorously strict parents. The media’s Asian representation movement is powerful and wonderful.

You know the feeling: Your friend just got an A in the class you got a B in, your roommate got an amazing paid internship over the summer, your best friend just got into a relationship. You want so badly to be completely happy for them because they deserve the best, but you just can’t.

Jordans have been, are currently, and always will be infinitely times better than Yeezys. They outcompete Yeezys aesthetically in quality and range, and in most sales metrics, despite Kanye’s tweets.

New, original crosswords will appear monthly. S

Ezra Cornell was a farmer. He was a scientist, a philanthropist, a politician, and a lover of nature, but on top of all that, he was a farmer.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, October 29 edition of the paper.

A nurse, dressed completely in navy-blue and gripping a clipboard, sprints down the hallway––in my direction, I assume. But my optimism proves short-lived, as she passes by my bed just as fast as I had gotten my hopes up.

Say it with me. Loud and proud.

As overachieving, hyper-competitive Cornellians, cultivating balance in our lives usually doesn’t make it to the top of our priority lists.

Here is a secret I have never shared with anyone: I haven’t paid for textbooks since sophomore year. I’m a senior this year.

Trump is determined to restore democracy in Venezuela. Mantras of egalitarianism and humanitarianism flood the American discourse surrounding the Venezuelan crisis.

The figure of James Baldwin has been buoyed in recent years by a revival across the liberal wings of the United States’ political, cultural, and intellectual establishment. Most notably, during remarks given at the dedication ceremony of the National Museum of African American History and Culture in 2016, former President Barack Obama quoted from Baldwin’s short story “Sonny’s Blues.” That same year, Raoul Peck’s Oscar-nominated film I Am Not Your Negro enjoyed widespread critical acclaim over its solemn presentation of the Civil Rights-era writer’s saliency to the present-day (A.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, October 15 edition of the paper.

Created by Monika Bandi ’19 and Gabe Ares ’19

Answers below

*

*

*

*

*

*

By Jeffrey Ho September 27, 2018

Biomedical research and engineering, genetics, biotech — these are all disciplines rising in popularity among research, academics and scientists, and with a similar goal in mind: they emphasize the use of multi-disciplinary teams to ensure quick “bench-to-bed” results which translate basic scientific research to the medical community and then to the patient. Yet these rising disciplines are gaining ground at such a fast pace that many scientists and physicians have begun to neglect an important aspect of translational research: the native and marginalized populations around the globe that are heavily involved in the medical research, yet rarely reap its benefits.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, September 24 edition of the paper.

New, original crosswords will appear monthly.

New, original crosswords will appear monthly.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, September 17 edition of the paper.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Tuesday, September 4 edition of the paper.

Meet us halfway and submit a caption for the first cartoon of the semester! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Wednesday, August 22 edition of the paper.

This past Friday, June 27, 2018, marked the 65th anniversary of the Korean Armistice Agreement, a ceasefire agreement signed in 1953 between North Korea and the United States/United Nations that (1) did not officially end the Korean War, (2) established the Demilitarized Zone at the 38th parallel as the de jure border between North and South Korea, and (3) did not include the input or signatures of any South Koreans. The anniversary underscored what has been an exciting, albeit precarious period of swift developments in the triangulated relations between the governments of North Korea, South Korea, and the United States in recent months.

Since when did NBA fans become so spoiled? All I see online is people kvetching about another “boring” finals rematch between the Golden State Warriors and the Cleveland Cavaliers and how Kevin Durant has ruined the NBA.

Finals week can bring a lot of things to the surface: the sudden motivation to learn everything, a seasonal caffeine addiction, an awe-inspiring general state of self-loathing. After barely making out alive from seven finals seasons, I have come to realize that finals week also brings out the economically irrational agent hidden in all of us.

Dear Freshman Brittany,

Welcome to Cornell! You’re going to change so much over the next three years, and I’m legitimately so excited for you.

I have no right to feel guilty when I tell a rocket scientist or a pre-med I’m an English major. And yet I can’t seem to ditch that ball-and-chain question that follows me everywhere I go: why am I doing this?

Congratulations to the winner of Cartoon Caption Contest #10 (who was also the winner of our last contest)! “Yeah, I had some BRBs left.”

Fruit has been on everyone’s mind throughout history. According to the Bible, the only reason humans even have the mental capacity to think about fruit was because Adam ate a fruit.

Coming into freshman year, I came to know a typical Ivy profile, a profile molded from a strict checklist and meticulously groomed to satisfy all its criteria ever since childhood. I began to notice consistent commonalities among a seemingly diverse community of academics.

As of today’s date — Tuesday, May 1, 2018 — I am officially accepting applications from any and all individuals or entities interested in becoming founding members of Liberty in South Korea (LiSK). Serious inquiries may be sent to [email protected] .

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, May 7 edition of the paper.

By Ethan Wu April 28, 2018

The Wall Street Journal editorial board traffics in baseless doubt-casting and bunk. The president seems delighted.

The answers to original crossword puzzles in the Cornell Daily Sun are posted monthly on Sunspots.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 30 edition of the paper.

“Just because you fight for something doesn’t mean you have to have a philosophical justification for it.”

By what was then the twelfth week of this semester, I had grown accustomed to 98% of the inane phrases which were tossed casually — as casually as one might toss a molotov cocktail — into the collective consciousness of my English/Comp Lit seminar. The ratio of neural/motor energy devoted to jotting down whatever convoluted statements followed the words, “This is important,” from one of professors’ mouths (it’s one of those rare two-professor courses) versus scrolling through Facebook and answering emails had gradually shifted in disproportionate favor of the latter.

People generally agree that music has an impact on mental health and our moods, whether through numerous studies that show correlations between music, relaxation and improved mental health, or through countless Twitter memes about sad Drake songs. Some people even program music around their lives, listening to certain music in the morning to pump themselves up for the day, or calming music at night to sleep.

The Marvel Cinematic Universe has done miraculous things, namely building a highly successful franchise with eighteen (and running) feature films, turning formerly B-list heroes into household names. Who had even heard of Tony Stark before his popular appearance in his successful solo movie, Iron Man?

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 23 edition of the paper.

A healthy person who begs for food is an insult to the generous farmer~ Ghanaian Proverb

Ava’s strongest memory of her father was the day he left. Memory is a weird thing, Ava thought as her toothbrush slowly crept into the inside of her jaws.

If you’re anything like me, you’ve probably had your share of derpy moments with those awkward and often embarrassing times when your face turns red and you let out a nervous chuckle. If you were anything like me during middle school… well, let’s just say that those moments did not make the sixth grade very pleasant.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 16 edition of the paper.

By Ethan Wu April 7, 2018

The national conversation on gun control is deeply confused. One question looms large: should the Second Amendment be repealed?

Strangers come to know me as, “that girl who brings disposable cameras to parties,” a tagline I’ll accept. Though tokens of a past seemingly devoid of technology, these unmistakable plastic machines have become pretty fundamental to my college experience.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, April 9 edition of the paper.

Sampling in hip hop and rap has been done over and over again, adding a layer of background vocals and richness to the beat. Samples come from a broad range of musical genres: DJ Khaled sampled Maria Maria by Carlos Santana for his hit song Wild Thoughts, and Drake sampled indie singer Snoh Aaelegra for his introspective number Do Not Disturb.

Just last week, Toys “R” Us announced that it would be closing its U.S. stores, and I genuinely felt sad about this — sadder than I did when my parents told ten-year-old me we would no longer be going to Blockbuster on Saturdays for our weekend movie nights (until a year and a half ago, I actually kept a Blockbuster membership card in my wallet). Perhaps this especially wistful reaction is due to the fact that not three blocks from my paternal grandparents’ house is a shopping plaza, at which there used to be a Toys “R” Us location.

Last Friday, the second Avengers: Infinity War trailer was released, and millions of nerds around the country immediately creamed their pants. Let’s analyze it.

New, original crosswords will appear monthly.

New, original crosswords will appear monthly.

One of my lovely friends—I don’t know what I would do without him—recently introduced me to “(No One Knows Me) Like the Piano,” a piece from Sampha’s debut album Process. The song’s title quite literally captures the essence of it, in which the British songwriter repeatedly croons, “No one knows me like the piano in my mother’s home.”

Like Sampha (“And you drop-topped the sky, oh you arrived when I was three years old”) and countless others, I began playing the piano at an early age—seven, to be exact.

Daydream for a moment and imagine that you’re standing in the wings of an auditorium, looking at the empty stage in front of you; the set pieces have been taken down, the lights give off a dim white glow, and it’s absolutely silent. You slowly walk forward, and you can hear your footsteps lightly thud and echo.

Olivia Faulhaber ’21: I will never forget the time that my family and I vacationed in Woodstock VT. We decided to take our bikes to Sugarbush Farms. However, the ride there was BRUTAL.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, March 26 edition of the paper.

I have a very peculiar taste when it comes to television. You won’t see me catching up on the latest Riverdale or binge-watching The Office.

“Colonialism imposed its control of the social production of wealth through military conquest and subsequent political dictatorship. But its most important area of domination was the mental universe of the colonised.” – Ngugi wa Thiong’o, Decolonising the Mind

Part II: Matatu in the A.M

Vacant eyes stared past Ava and onto some unseen distance. Her mother, Charity, sat in a rocking chair in the common area near the staircase.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, March 19 edition of the paper.

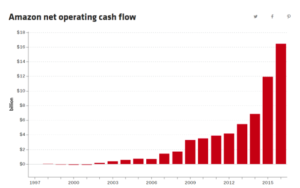

It is hard to think of an aspect of our material lives that Amazon has not touched. Amazon has become such a ubiquitous and practically tangible presence despite being based entirely online.

A new card game has been going around lately, invented by our very own Cornellian, Kevin Zhang 21’. The game Fish is a mix between Go Fish and Kemps, except it is much more difficult. My friend group and I have been obsessed with this game this past month, and gladly sacrifice way too much of our studying time to play Fish.

According to the World Happiness Report, Denmark, after Norway took the crown, is listed as the second happiest place in the world. Hearing this, it is easy for one to flee to the Nordic countries in hopes of getting a taste of what this “happiness” feels like.

This week, many people criticized the NCAA for its treatment of college basketball players. LeBron James called the NCAA “corrupt.” Stan Van Gundy, the coach of the Charlotte Hornets, remarked that they there were the “worst organization” and labeled their actions as “racist.” This criticism emerged after a report revealed that dozens of players had been paid and given loans as compensation for their play.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, March 12 edition of the paper.

With an open mind and two sides of the story, you’re bound to learn something new.

Welcome to the zoo!

The Crossing is a micronovel in the genre of Afrofuturism written in honor of Black History Month. It will be published in excerpts every second Wednesday.

By April Ye February 27, 2018

For those who still haven’t quite mentally prepared themselves for adulthood yet (read: me), this could be quite a jostling thought: where exactly is home now? Prior to coming to Cornell, I was so caught up in the frenzy of excitement and eagerness to explore the newfound limits of college and independence that I never stopped to consider the consequences of the transition: once I moved out, would my definition of “home” change?

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, March 5 edition of the paper.

Sleep deprivation: it is a problem that students across the nation complain about almost daily. Personally, I can’t get through a conversation with someone without the words “I’m so tired” coming up, not to mention the slew of other complaints of work and extracurriculars contributing to the issue.

By Jeffrey Ho February 22, 2018

With the 2018 Winter Olympics well underway, many have found inspiration to hit the gym and keep their New Year’s resolution well and alive. Here’s a playlist inspired by the music of the Olympics, whether it’s a song endorsed by athletes themselves or played during competition.

Meet us halfway and submit a caption for this week’s cartoon! The Sun staff will vote and the winning caption — along with the winner’s name — will appear in the Monday, February 26 edition of the paper.

As we speak, college students worldwide pull out their shotskis and ice luge molds in celebration of the most riveting quadrennial exercise in patriotism, team spirit, and demolition of self-worth—the Winter Olympics. This year’s games are being held in Pyeongchang, South Korea, a city of 40,000, of which only 35.6% were interested in the Winter Olympics, according to a survey taken last April by the South Korean Ministry of Culture, Sports and Tourism.

“Look, this is the Bill and Melinda Gates building,” my dad said to my mom for the fifth time as we drove past Gates Hall on our way to East Hill Plaza. My parents don’t get to visit often, and I don’t blame them, since they live 2,000 miles away.

Western culture loves to rank everything. From foods to sport teams to cities, we obsess over figuring out the best thing, the second best thing, and so on.

I haven’t seen Black Panther yet, but I know enough of the story’s basic premise — what might an African nation, untouched by centuries of colonialism and the transatlantic slave trade, look like in the 20th/21st century? — to use it as a generative point of speculation within my own interests in the history of the Korean War and its aftermath.

By Ethan Wu February 15, 2018

The vile regime to the north is putting on a pretty face for the Olympics. Don’t be fooled.

With an open mind and two sides of the story, you’re bound to learn something new. Welcome to the zoo!

I painted my nails red for Valentine’s Day. Very cliché, I know.

Cornell has some great off-campus programs to offer, one of them being Cornell in Washington. This program offers students the opportunity to live, study and work in Washington, D.C., which means you get to kill three birds with one stone by earning Cornell credits, getting work experience and touristing.

Jacqueline Quach ’19: The flashy figure skating outfits! Where else can one appreciate such brightly colored, such meticulously designed and bedazzled fashions?

This article represents the first in a hopefully long series of articles which aims to address controversial topics in an open and civil manner here in Sunspots. The name was chosen carefully: the agora, the marketplace of ancient Athens, was at once a place where material goods were exchanged and where ideas and conflicting viewpoints could be expressed in the open air for all to hear and criticize.

By Lev Akabas February 12, 2018

Forrest Gump → Forrest Dump

The past couple months have seen some exciting new music releases in the hip hop world. Between Drake’s new singles, Migos new album and so many more new projects coming out, there’s a lot to digest and review.

By Ethan Wu February 9, 2018

America’s tech titans are stifling competition, skirting regulators and harming democracy. Time to break them up.

It is difficult to grapple with our complex understanding of the past. Sometimes we remember an event.

Ah, syllabus week. The time to lounge around with friends, partake in that Tuesday karaoke night at Loco, embark on that spontaneous trip to Niagara Falls with your friends—these are the good days.

Too often, true crime podcasts fetishize or take light of heinous human actions. I’ll admit, I’ve listened to many – and have even written about them.

Like any sleep-deprived college student earning a degree in Procrastination, I often convince myself I need a study break, only to find myself panicking two hours later because I spent too much time (1) reading about the endless antics of well-dressed but not-so-well-behaved Lapo Elkann (decadent heir to the Fiat fortune), (2) browsing the sale sections of online clothing retailers that shall remain unnamed (for the safety of your wallet) or (3) poring over the exceptional articles written by the Blogs section. However, as of late, I’ve noticed that I’ve been reining in those study breaks pretty well, so that the most they’ve gone on for is maybe half an hour.

First of all, why the bloody hell is this game called football if the least talented player is the kicker? But before I get too miffed, I’d like to tell you all about how this year’s American Football Championship Match will “go down” as you Americans say it.

A lot of students choose the spring semester to study abroad or take advantage of off-campus opportunities such as Cornell in Washington. As an international student, I’ve essentially been “studying abroad” since freshman year but this spring I decided to take a break from the Ithaca cold while also getting work experience and Cornell credits by participating in the Cornell in Washington Program.

Since my first purchase of MUJI pens back in 2013, I’ve personally witnessed an exponential increase in the number of people carrying around the signature MUJI clear-bodied gel pens in class. While many of you probably have also been introduced to this brand’s signature stationery, there is actually a lot more to MUJI than meets the eye.

By Ethan Wu December 15, 2017

This past year offered gloom and uncertainty—and inspiration. A brief, hopeful retrospective on 2017.

By Nuri Yi December 15, 2017

We’re in that strange twilight zone between the end of classes and going home: is it finals week or is it the end of all things looming? I couldn’t tell you how the time has been passing; all I know is that I wake up, work-work-work (or try, at least), forget to eat, get too tired to continue working, and go to bed at strange hours, the only constant in my life being the fact that I’m perpetually falling behind the rigorous study schedule I devised for myself in a last-ditch attempt to #savemysemester.

Standing beneath McGraw Tower at midnight is akin to experiencing the prolonged death throes of an eternity. Every day becomes as the instar of all time en miniature.

By Grace Chen December 13, 2017

I hope everyone had an amazing Thanksgiving Break! Like 80% of Cornell’s freshman population, I headed over to New York City for a nice and homey friendsgiving.

By April Ye December 10, 2017

As we embark upon the homestretch of this semester, I often find myself spacing out over my usual Temple of Zeus iced mocha. Weirdly enough, I hadn’t even noticed how frequent my coffee consumption was until a friend from home pointed it out via cross-country Facetime—every time we talked, I seemed to have a convenient cup of coffee within hand’s reach.

In 2015, Jay-Z purchased Tidal for a cool 56 million dollars, touting it as a streaming platform “controlled by the artists”. Now, his Tidal holdings have boosted his net worth to make him the 2nd richest hip hop artist in the world, right behind Sean Combs and surpassing Dr. Dre.

By Ethan Wu November 30, 2017

The push to expose sexual assault could give way to a long-awaited reckoning with America’s sexist rot. But if #MeToo becomes a mania, it might not.

On November 15, the military took over my country’s main broadcasting station, the Zimbabwe Broadcasting Cooperation, and announced that it had put our president of 37 long years under house arrest. A week later on the 21st, President Mugabe turned in his resignation letter just as the impeachment process in Parliament began.

Women’s sports across the country are stuck in an vicious cycle, and an example of this cycle can be found right here on campus.

There is no question that, at an increasingly fast rate, technology and media have advanced significantly. Facebook, Twitter, Instagram, Internet, iMessage, text messaging, and other various forms of communication can now all reside on a single smartphone.

I’m not sure when I got my first pin, but the earliest documented proof I could find of me wearing a pin is from May 14, 2000. In the picture, my parents are conducting a mini-photoshoot at home with my older sister and two-year-old self, and you can see a tiny pair of red sunglasses pinned to the top of my pink cardigan:

To this day, I still have and frequently wear that red sunglasses pin, but it’s fair to say that my pin collection has since expanded.

By Ethan Wu November 13, 2017

Robert Mueller has investigated Russian meddling with diligence and professionalism. Firing him would be disastrous.

Can’t decide where to eat today? We’ve got you covered.

I glare at myself in the mirror. Maybe if I stare at my reflection long enough, critically enough, I’ll finally see myself the way the U.S. government sees me: white.

Noah Harrelson ‘21: Risley’s overnight oats, that sweet nectar of Gods. As I eat, the world stops.

In late September 2016, Houston Rockets coach Mike D’Antoni announced that his star player, James Harden, would be switching positions to play point guard. This seemed like a peculiar decision at first.

As I get older and wiser (all 21 years and six months), I’ve come to realize that although I am an American, America (or my country) was not made for me. This land of the free was made on the backs of my ancestors who did not enjoy such freedoms. Having grown up in mostly white environments and choosing to attend a predominantly white university, I’ve become accustomed to being the only black girl in the room.

As the weather gets colder and the wind shows its wrath more and more, it becomes really difficult to walk around campus every day. It can also be especially cumbersome during these chilly times to keep our skin smooth and soft.

3:00 A.M. is high time for a deflated, depressed-looking bag of Cheetos. My mind steers me like a sleepwalker down a flight of stairs and into the bowels of my dorm.

While Cornell is known for its superb dining hall food, Ithaca has many of its own culinary gems, one of which is Louie’s Lunch Truck. A favorite among Cornellians, Louie’s is that place you go to when you’ve got those late night or post-partying greasy food cravings.

By Tony Li October 30, 2017

Deciding what, when, and where to eat may seem like a simple task at first. But when our schedule becomes busy with clubs & classes, overwhelmed by personal circumstances, or just unorganized in general, proper and balanced eating habits can often take a backseat.

While I will never understand 90% of the logic behind the store layout of Ithaca’s Wegmans (e.g. why the dried noodles must appear in seven separate aisles), I will admit that the Wegmanites got one thing right: the strategic placement of the avocado bags. Their perpetual position in a giant wooden crate by the entrance has permitted me to develop somewhat of an avocado dependency in recent years.

I thought of some really simple, fun recipes that everyone should try this fall season! To kick things off, I’ll start with two takes on a seasonal favorite: the pumpkin spice latté.

Engineering = Warheads

For some reason, Mech-E’s and Chem-E’s think they’re at war with every other major at Cornell, and won’t go more than two minutes without reminding you that they’re engineers and that your major is inferior. They treat every project or interview like it’s a life-or-death situation and you think they might explode at any given moment.

By Ethan Wu October 27, 2017

Tribal politics have paralyzed America. Amid our division, radical centrism offers hope of renewal.

This year, Cardi B exploded onto the rap scene with “Bodak Yellow” after remaining relatively unknown, though she did have a large Instagram following and became a regular cast member on a reality TV show, Love & Hip Hop, New York, in 2015. Due to “Bodak Yellow”’s success, Cardi B became the first female rapper to, unassisted, hit Number 1 on the Billboard charts (other female rappers only reached Number 1 with features on their songs).

Welcome back to my list of cool, creative, and borderline exotic beauty products! I’m going to be giving reviews on some popular face masks in this article.

By Nuri Yi October 24, 2017

I have something to confess: I love Tinder. And, disclaimer (because it’s necessary): I’m not hooking up with anyone on it.

Last spring’s union election campaign may have ended with a disappointing result for the collective rights of Cornell’s graduate students, but Cornell Graduate Students United (CGSU) has continued to fight. In the past weeks, members of CGSU have been asking fellow graduate students at Cornell to vote about the future of their organizing strategy and the possibility of another election attempt.

I went to my friend’s event Tuesday night, a Hillel event, titled “A Funny Thing Happened On My Way to the Middle East,” in which Joel Chasnoff spoke about his life story, and in particular, his relationship to Israel. What started as a stand up bit—typical in its delivery, ingenuity, and laugh-generating ability but atypical in its Jewish-oriented humor—turned into a serious opportunity to discuss Israel in a safe space among mostly Jewish students.

By April Ye October 20, 2017

Upon a cursory brows—ha, pun intended—everything can seem so easy. That is, until you’ve actually been through the process yourself.

For international students, moving to a new country with a different language and culture takes a big adjustment and relearning of social cues. One of the biggest worries as a black international student is whether or not you will find beauty products that cater to your hair texture and that understand your skin.

Thus far in my twenty-year tenure on this planet, I’ve traveled to quite a few places–within the United States, I’ve been to Portland (Oregon), Reno, Yosemite, Las Vegas, Niagara Falls, New York City, Boston, and Atlanta. Internationally, I’ve been to France, Switzerland, Lichtenstein, Germany, Austria, Italy, and Taiwan.

With the chilly weather and colorful leaves rolling into the Ithaca area, there’s no doubt that fall season is upon us. And with the fall weather and ambiance comes the obvious pumpkin obsession: pumpkin muffins, pumpkin pies (who could forget Patty’s delicious pumpkin pies?), and, of course, pumpkin spice lattes.

With an open mind and two sides of the story, you’re bound to learn something new. Welcome to the zoo!

A spectre is haunting America: the spectre of communism. In a world where more and more tasks are being automated, and more and more people are seeing the skills that separate them from the lower rungs of society reduced to a few lines of code on a computer, more and more people are starting to ask: what makes me more valuable to the company than the guy two floors down who makes half as much as I do?

Korean cosmetics have been gaining popularity in recent years, and many of the products that used to be sold exclusively in Korea have started to become more accessible here in the US. From 20-step skincare routines to Chateau Labiotte lip tints, there’s definitely a lot going on with Korean beauty that everyone can experiment with.

By Yang Lu October 6, 2017

It’s a tumultuous time to be Cornell student. A University first founded on the principle of “any person, any study” has proven time and time again that the students themselves do not live up to these words.

Although there has been significant progress in recent years, there is still a lack of substantial representation of women and people of color in the entertainment industry. With that being said, podcasts are a cheap, readily disseminated way to share stories and cultural experiences.

With an open mind and two sides of the story, you’re bound to learn something new. Welcome to the zoo!

For this semester’s first installment of “Office Hours,” a series of interviews with prominent personalities on Cornell’s campus, Sunspots writer Gabriel Ares sat down for a chat with Applied Engineering Physics Professor Lena Kourkoutis. In the interview below, which has been edited for clarity, Kourkoutis talks about a range of topics, from electron microscopy–a technique that allows her to see the atomic structure of objects–to outreach to women in STEM.

See, Trump, I said it. Just like you wanted me to.

On September 29, The Daily Caller claimed that Black Students United (BSU) at Cornell had insinuated in their list of demands to President Pollack on September 20 that Cornell “is letting in too many African students.” Upon seeing this headline, I dismissed the article as the click bait material straight out of a troll handbook. But because college has taught me to question everything and dismiss nothing, I took another careful look at BSU’s demands.

This past summer, swaths of bright college students armed with alacrity sauntered into corporate headquarters and satellite offices, hoping to assert themselves in prestigious and difficult internships. For many of us, this time period was nerve wracking and intense.

Ithaca is known for its grocery stores—each with its own distinctive personality. Which one are you?

What would it be like to return to a home that no longer recognized you? Maybe the people you knew have packed up and left, maybe they are no longer on speaking terms, and you no longer feel at ease.

By Tony Li September 28, 2017

A week ago, my roommate asked me if he could use my Netflix account. At the time, I didn’t think much of it.

If Ithaca possessed a “spirit food,” it would be the apple. After living in Ithaca for the past three years, I have consumed way too many apples in solid, liquid, and in-between forms. In their own subtle way, I feel as if apples define Ithaca just as much as the gorges or the freezing cold winters.

There are so many great things to do in Ithaca and I’ve certainly collected my fair share of memories and moments that have helped me to call this place home. I remember going to Taughannock Falls as a kid; I’ve been to the Ice, dog, and apple festivals; and I’ve spent days studying in the little coffee shops in The Commons and going to poetry readings at Buffalo Books (often because I was forced to trek down there when a professor didn’t want to support the Capitalist Pigs at the Cornell store).

April: Amidst the hustle and bustle—the only trace of New York City here in Ithaca—it feels liberating to venture outside every now and then to explore Ithaca and recharge in the loving womb of nature. Don’t let the “there’s nothing to do, Cornell’s in the middle of nowhere” eye-roll mislead you.

President Donald Trump is in many ways the antithesis of former President Barack Obama. In the beginning months of his presidency, Trump has attempted to do away with many of Obama’s signature policies, including the Patient Protection and Affordable Care Act, the Paris Climate Accord, and the Deferred Action for Childhood Arrivals (DACA) program.

So, if time is really money, this hangs on the notion that time must indeed be real. Which then, arguably, hangs on the notion that money is inherently real as well.

The Cornell Daily Sun’s well-known list of “161 Things Every Cornellian Should Do” is very comprehensive and covers most of the essential Big Red experiences, but not all of them. So we asked our writers and our readers to think of some things that they would add to the list.

Since you readers seemed to enjoy my first article on this topic so much, I’ve come back with a second installment to this series with just as interesting and spooky factoids! Here we go:

1) Whispering Bench

When I was doing research for my other article last semester, I stumbled onto a thread on College Confidential, in which there was mention of a “whispering bench near Goldwin Smith.” However, after scouring the internet, I could not find any other website or article that referenced this bench!

The passing of a loved one is never easy. It’s even worse when it happens during prelim season and a continent away from home.

At this point in my budding blog I should probably add that these posts are not jokes—they are meant to highlight the contradictions surrounding campus life. Ahh, The Greek Reformer.

In an ideal world, flossing would be a part of everyone’s hygiene routine. At least that’s according to the American Dental Association.

That quote about being a tiny speck of dust in the infinite span of the universe—intended to be a comforting reminder that our actions do not merit the importance we delude ourselves into believing they do, and that we should really just relax—is actually quite demoralizing. Maybe it’s the leftover traces of teen angst that have dutifully followed me into my twenties, maybe it’s just how I’m feeling this particular rainy Thursday night—but that quote just makes me kind of sad.

By April Ye September 15, 2017

Taking a step back, I can’t believe we’re already on week 4. My groggy brain tries to do the countdown of how many weeks left until the end of the semester.

There is something to be said about people-watching; something to be said about sitting in Olin Library staring out at the people playing Frisbee in the Arts Quad, or perhaps walking down Ho Plaza figuring out how to dodge the quarter card mania properly (NOT me though, I love all of your quarter cards… STAY #woke). From an outsider looking in it’s interesting to ponder, even for a millisecond, the thought processes that encapsulate another person’s mind.

“’Εν ἀρχή ῆν ὁ λὀγος, καì ὁ λóγος ῆν πρòς τòν θεóν, καì θεòς ῆν ὁ λóγος. οὗτος ῆν ἐν ἀρχὴ πρòς τòν θεóν.

By Tony Li September 11, 2017

A few weeks ago, I received the best haircut of my life. What were my benchmarks?

By Yang Lu September 11, 2017

This piece was written at the time of—and in direct response to—the “Unite the Right” rally and ensuing violence that took place in Charlottesville, Virginia on Saturday, August 12th. Before you read this article, I suggest that you watch this video from Vice News first.

Since Trump rescinded the DREAM Act a few days ago, a number of articles have appeared on the internet citing the extreme cruelty of his decision. Many of these articles make their point by showing a Hispanic male in their early 20s doing something admirable—graduating as Valedictorian from high school, saving people’s lives during Hurricane Harvey, researching a cure for cancer—and juxtaposing it with the inevitable fate Trump has forced upon them just to gain a few political points: being deported to a country they have never known.

I am not ashamed to admit it, but I am an avid Bachelor/Bachelorette/Bachelor in Paradise watcher, debriefer, and obsessor. For the last six months or so, my Monday and Tuesday nights have been dedicated to watching who gets the first impression rose, the ever-coveted one-on-one date, and finally the Neil Lane ring. The franchise’s premise is a bit unorthodox; one person dates 25 people over the course of about 12 weeks in the hopes of getting engaged, then weeks later the Bachelor/Bachelorette rejects get shipped off to Mexico to find love in Paradise.

By Grace Chen September 8, 2017

Whether you love to spend hours on dorm decoration or just want to do the bare minimum, it is undeniable that loving your dorm room is very important. After all, how comfortable you are with your personal space determines how much sleep you get, which affects your ability to get up for those 8am classes, which determines your GPA.

The violence that erupted in Charlottesville, Va. this August turned the idyllic town on the foothills of the Blue Ridge Mountains into ground-zero of the debate on statues and white supremacy in America.

Over the summer, I managed to save up for a trip to California, one of the places in America celebrated for its liberalism and openness. Ignoring the sinking feeling that few other tourists would look like me, I set about to explore the Bay Area.

Before the contemporary hipster existed, there was the hippie of the 1960s. (Ironically, the term “hippie” was derived from the word “hipster,” which referred to the jazz cats of the 1940s.) Perhaps the most notable year for any hippie is 1967, whenduring which the Summer of Love took place in San Francisco.

It really is something to chuckle at, the way Cornell speaks about liberal arts. Specifically within the College of Arts and Sciences, there exists an issue with the rhetoric surrounding our breadth and depth requirements, which I argue stems from our grade-centered education.

Sasha Chanko ‘19: Eat your f***ing breakfast. Wake up, have a bar or yogurt or something small in the dining hall.

Part I: The Drive Up

This entire summer, I’ve been dreading the day that Fall 2017 starts because it will signal the beginning of the second half of my college experience. As I’m honing in on exactly what I should do at the start of this second half, I’ve been reminiscing and reconsidering all the things I did at the start of the first half, by which I mean: freshman year.

Cornell is a difficult place – colloquially, we are known as the easiest Ivy to get into… but the hardest to graduate from. While many of you are among the swaths of high school valedictorians, science fair winners and speech and debate aficionados, all of you will certainly fail at some point in your college careers.

One of my formative orientation week events was Big Red Ball. For those of you who don’t know what Big Red Ball is, don’t worry—it’s really simple.

When I teetered into my dorm room on the first day, weighed down by three bags I had lugged across the country, I wasn’t inspired by any sense of new beginning despite all the people offering me their collegiate wisdom and telling me that my life had just begun. I missed home, I missed Mom, I felt like I was still just me, packed up and shipped 3000 miles away.

If you’re not one of those people who shows up to Ithaca waaaaay too excited about going to their first college party, have no fear. Your options for activities during O-Week are endless!

By Tony Li August 18, 2017

Understanding Surroundings through Design Thinking

Last week, Sarah Huckabee Sanders, the new White House Press Secretary, read a 9-year-old boy’s letter to President Trump during a press briefing. This lucky 9-year-old boy is Dylan Harbin, also known by the nickname Pickle.

Across three Batman movies, five movies with cool-sounding one-word titles, and one movie you’ve probably never heard of, director Christopher Nolan has developed a distinctive style. So, with his latest film, Dunkirk, hitting theaters today, we’re going to answer a very important question.

For how many more finals do you anticipate the two teams will be the Warriors and Cavs (i.e. the next 3,4,5 years?)

Basically the Warriors’ entire roster is entering free-agency this offseason. Stephen Curry and Kevin Durant are going to do what it takes to both re-sign, but what about the other guys?

When the NBA season came to a close on Monday night, I had too many thoughts to sort out, so I decided to let my friends do it for me by sending me questions. Below are my answers to 10 questions about the 2017 NBA Finals, ranging from most simple to most complex.

VIDEO

David Pizarro has taught Introduction to Psychology and a number of other seminars since becoming an associate professor in 2012, and his research on moral judgement and emotion has been published in countless places, including an article for The Guardian that he co-wrote last month. He was nice enough to be the guest for my first Cornell Daily Sun podcast, during which he discussed his research, shared his thoughts on robots, and answered ten “Speed Round” questions.

When I graduated high school, I wrote a farewell piece in the school paper; it came easy, words were flowing without obstacles, I had a lot to say. Four years later, I still have a lot to say; however, this is one of those very few times when I felt that there might not be enough words, or that they will be too small and timid, too controlled, too human.

For our second installment of “Office Hours,” a series of interviews with prominent personalities on Cornell’s campus, Sunspots writer Andrew Shi talked with with Performing and Media Arts Professor Bruce Levitt, who has taught at Cornell since 1986 and is involved with Phoenix Players Theatre Group (PPTG), a prison theatre group at Auburn Correctional Facility.

You’ve worked with PPTG since 2010.

Atticus Finch is racist. That’s the shocking revelation in Harper Lee’s sequel to the beloved classic To Kill a Mockingbird.

As a college student, it’s important to be aware and take advantage of the student discounts that places like clothing companies, restaurants and especially museums offer, because it’s going to be more than forty years until you can get a senior discount…forty-plus years of dreary adulthood in which you are expected to pay full price for everything—the horror! Seriously though, it’s always nice to save some money, so I whenever I go to a museum, I have my Cornell ID ready.

People know Ithaca for its beauty. When I first visited Cornell in the summer of 2014, I was struck by the seemingly endless verdant grass on the Arts Quad and the sea of trees that surround the school.

Like most Cornellians, I find that during the school year, amidst all the prelims and deadlines, it can be hard to set aside some time to treat myself and take things slow, which is why I decided to indulge in food, museums, and strolling around when I spent my Spring Break in New York City. I won’t be writing about every experience I had – only the ones I found to be interesting and fun.

For our first installment of “Office Hours,” a series of interviews with prominent personalities on Cornell’s campus, Sunspots writer Bruno Avritzer sat down for a chat with Computer Science Professor Walker White, Director of the Cornell Game Design Initiative. In the interview below, which has been edited for clarity, White shares his thoughts on why gaming may or may not be viable as a college sport.

You did it. After countless, grueling months spent slogging uphill (physically, intellectually and emotionally) in sleet and snow, you’ve finally made it to spring—and oh my god that summer internship is so close you can practically taste it.

One of the most frequently cited arguments in favor of affirmative action practices at universities is that they help those with societal disadvantages succeed. Yet, by propagating stereotypes about the relative achievement of certain classes of individuals, affirmative action policies have perpetuated discrimination on the basis of race.

For our first installment of “Office Hours,” a series of interviews with prominent personalities on Cornell’s campus, Sunspots writer Bruno Avritzer sat down for a chat with Computer Science Professor Walker White, Director of the Cornell Game Design Initiative. In the interview below, which has been edited for clarity, White shares his thoughts on the global popularity of eSports, their potential as spectator sports and comparisons between certain video games and sports like football.

This NBA season, not a single rookie who played more than half of his team’s games averaged at least nine points per game while shooting at least 46%. For context, those were the 2016-17 statistics of 35-year-old defensive-specialist Tony Allen.

Our culture is sharing. Not sharing, with respect to giving to others, but sharing online.

With an open mind and two sides of the story, you’re bound to learn something new. Welcome to the zoo!

Usually I try to write something with facts, figures and opinions, but this time around I’m going to do something a little bit different. I’m going to talk about my personal experience with mental health.

Vladimir Nabokov first appeared to me as a stranger’s name on a Cornell t-shirt. A quick search online showed me that he’s a big deal—big enough to be printed on the same shirt as Ginsburg, Sagan and Morrison.

In the first weeks of his term, Trump issued a great many executive orders that have caused a lot of outcry and hurt a lot of people. He tried to ban Muslims from coming to the United States, raised border security and cut down financial regulations.

Trigger Warning: Potential Damage to Fragile Egos

As you might’ve figured out, my blogging technique is pretty straightforward: something happens to me – something simple, everyday, insignificant to history or to my neighbors but exceptional to me, less meaningful that I build it up to be – and I write about it. And since I went to Los Angeles for spring break last week, that is what I am writing about today.

“WIr sind doch nunmehr gantz / ja mehr alß gantz vertorben. Der frechen Völcker schar / die rasende Posaun /

It is the most logical thing in the world to yearn for the rigidity of the medieval cosmology, the moral landscape to which a stonemason, manuscript illuminator or painter could turn for artistic solace, and from whose ethereal, luminescent matter parabolic universes could take shape.

Over spring break, I had the opportunity to purchase my first car. The salesman at the dealership told my father and me that if I was the sole owner of the car, I would have to pay a lot of money for automobile insurance—compared to a “normal” adult. My dad and I eventually decided to be co-owners of the vehicle in order to save money through the insurance plan, since my father is cheaper to insure.

There are many things that literally everyone on Earth hates, such as airplane seats without flaps to rest your head, Hayden Christensen’s performance in the Star Wars prequels and those stairs leading to the footbridge at Cornell that are the worst possible length – it’s uncomfortable to go one step per stair and it’s even more uncomfortable to go two steps per stair. There aren’t many things that literally everyone on Earth loves, but one of those things is March Madness, the NCAA basketball tournament.

By Yang Lu April 4, 2017